If you're renting now, you most probably dream of having your own house one day. In fact, you’re probably already looking into buying a property in your name right now. So aside from finding that perfect dream home, what else do you have to prepare for in buying your own place of residence? Here are 8 important reminders before making that renter-owner transition:

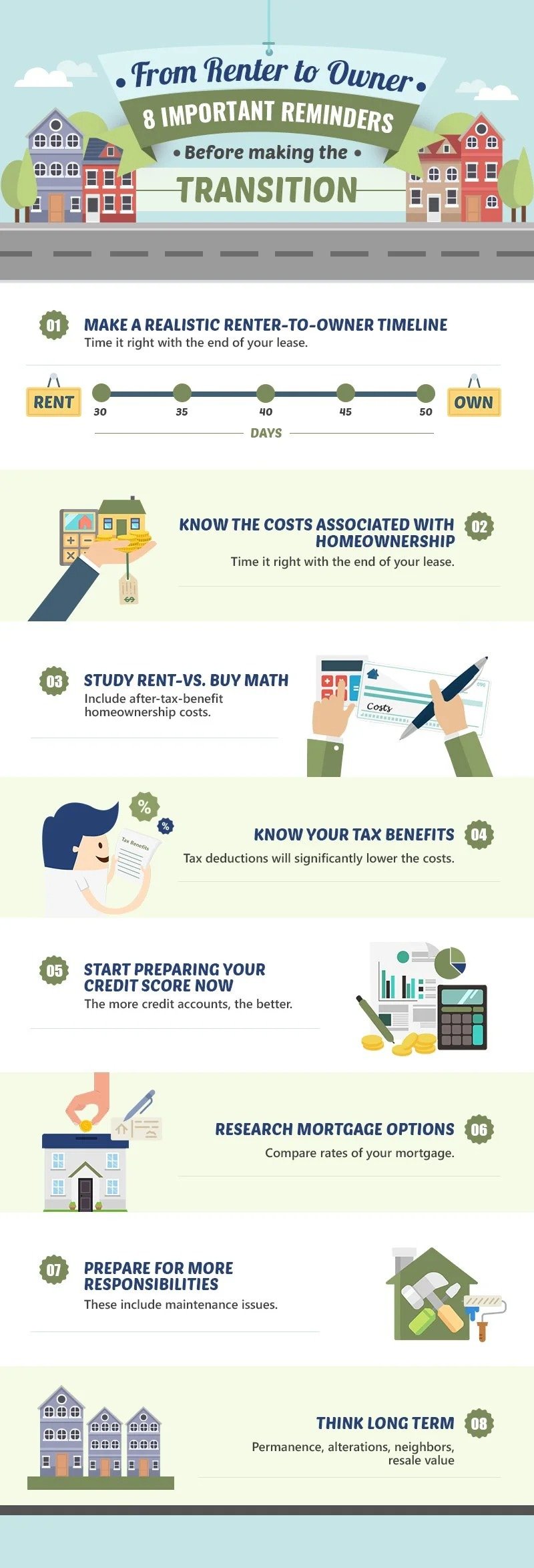

1. Make a Realistic Renter-to-Owner Timeline

After the tedious task of searching and even after your seller accepts your offer, you may think that the job is done. You're move-in ready! Not just yet. Be reminded that it may take around 30-50 days to close a home. You have to make sure that you time it right with the end of your lease. You don’t want it to be a renter-homeless-owner story!

2. Know the costs associated with homeownership

Costs, costs, costs! There’s a lot more to pay for upfront than just a security deposit as a renter—from deposits, home loan origination, title insurance, land surveys, home inspection, insurance escrow, appraisal, among others. Then, of course, you have to consider mortgages, home association dues, etc., in the long run.

3. Study Rent vs. Buy Math

More costs mean more math. This will be more than just rental payment vs. P.I.T.I. A more accurate comparison will also include after-tax-benefit homeownership costs and rent costs.

4. Know Your Tax Benefits

With all these costs, don’t worry, your tax deductions will significantly lower the costs of homeownership. Mortgage interest and property taxes will be deductible in filing annual tax returns, and reduce your taxable income.

5. Start preparing your credit score now

In getting the best mortgages, credit scores are very important. Those who lend want reliable and on-time payers, after all. If you only have one credit card, start getting more now, while you have time to grow your credit score. More credit accounts are seen as better.

6. Research mortgage options

You can’t only shop for the best-fitting home for you, but also the best-fitting lender, too. Compare rates of your mortgage based on your loan type, location, purchase price, down payment, and, as mentioned earlier, credit history.

7. Prepare for more responsibilities

These include maintenance issues from the roof of your home down to its very foundation. Set up insurance and even an emergency fund for these responsibilities.

8. Think long term

Consider the fixed features of the home, such as location. Think of the things you may want to alter in the long run, even take note that the neighbors you will have in this new home may be your neighbors for life, and if need be, think about the property’s resale value.